INVESTOR'S RESOURCE »

It is no mystery that owning a Denver rental property is a great way to build long-term wealth and even financial freedom. From our experience, most people have at the very minimum considered the idea of purchasing an investment property in the Denver metro area. However, many don’t know where to start or even how to determine if a specific property makes sense as a rental. Our goal with this short introductory article on Denver investment properties is to give you the foundation to start being able to recognize if a property would make sense as rental.

The first thing to keep in mind when considering an investment property is that you’re not buying this home to live in. This means you should not have any emotional attachment to the transaction or property. You must determine what your goal is with the property and only focus on that goal. This would naturally mean the next area of focus when buying a Denver investment property is determining what your goal is.

In my opinion, there is an important decision to make when buying an investment property. Will it be a long-term or a short-term investment? The best example of a short-term investment property would be a fix and flip. The best example of a long-term investment would be a rental property. For this article, we’re going to focus on long-term rental properties. We’ll share another article in the future focusing on short-term fix and flip properties.

Once you’ve decided you’re going to be purchasing a property with the goal of renting and holding the property, you need to get even more focused on your goals. The two main benefits of a long-term rental property are monthly cash flow and long-term appreciation. The first, cash flow, is definitely the area you have more control over and ability to predict, whereas appreciation is mostly out of your control and occurs more naturally with time. Before you even start looking at potential rental properties across Denver, you must first understand how to calculate and determine potential cash flow.

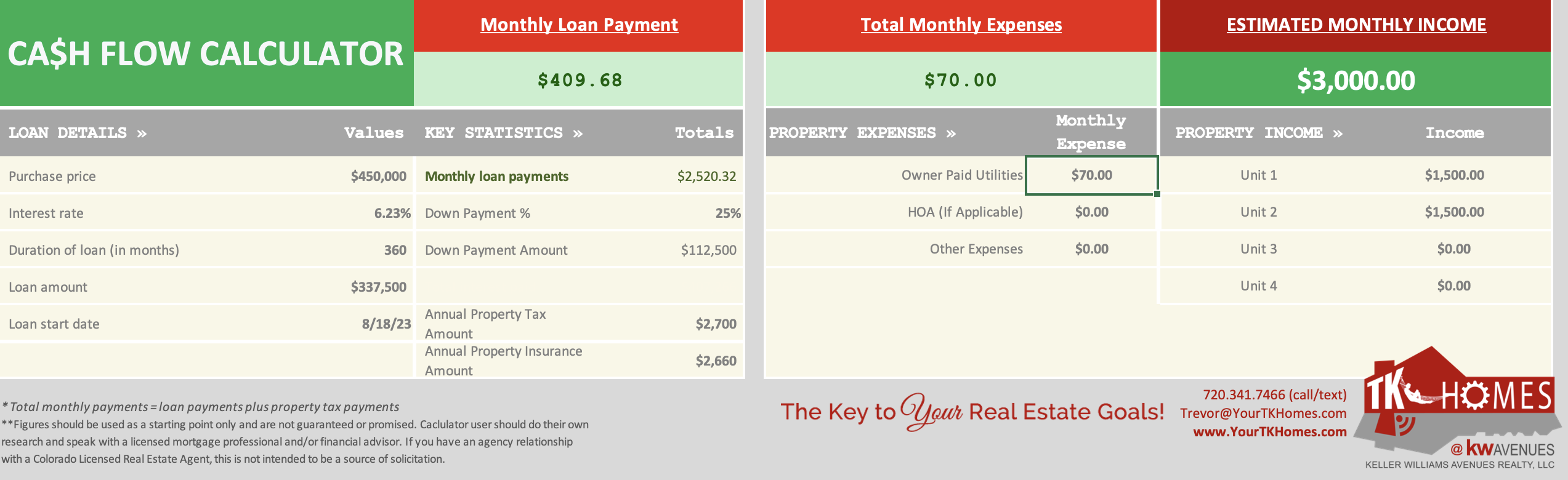

For this article, we’re going to assume that you’re purchasing the home with financing. There are two things to mention when financing an investment property. 1. You will be required by the lender and loan program to put down a minimum of 25%, and 2. Your interest rate will be higher than financing on a primary home, usually about 1% higher. This is important to ensure you’re calculating your monthly expenses correctly.

Below are the costs you will have as a landlord that will eat into your monthly cash flow:

» Mortgage Payment, including property taxes, insurance, principal, and interest

» Water & Sewer (this utility is usually a homeowner expense, due to the fact that it goes with the property and not an individual like electric or gas, if it’s not paid a lien can be placed on the home vs. connected to an individual’s credit)

» HOA (if in an HOA community, the HOA is also able to place a lien on a property if the HOA fee isn’t paid, which is why it’s usually a landlord/owner’s expense)

When calculating your cash flow, it is important to understand what the monthly rate is for each of the above items. If you don’t have exact figures for the item, such as water and sewer, it’s best to use a higher figure to ensure you’re ready for worse-case scenarios after you own the property.

The next step to determine your monthly cash flow is to figure out what the property might rent for. For this, we would recommend spending some time on Zillow. You can start by looking up the specific property in question and review its rent Zestimate. Now, we never recommend homeowners use the Zillow Zestimate for determining their home’s value, but we have found Zillow to be much more accurate with their rent Zestimates. Once you have that, look for similar rentals around the property. We would look in a 5-mile radius at similar property types, for example, homes vs. homes, townhomes vs. townhomes, etc. If you’re seeing rents similar to the Zestimate, you can assume that is going to be a good starting point for rent, plus or minus a few hundred.

Now that you know your monthly expenses for the property and the estimated monthly rental rate, you can calculate your cash flow. You do this by simply taking the rent amount and subtracting your monthly expenses; hopefully, this figure is positive and not negative. If it is negative, the best thing to do is either adjust your down payment to reduce monthly expenses or walk away. If it’s positive, you might have a good investment opportunity.

There are a couple things to remember when looking at Denver area investment properties. First, you need to remember that like rent, rates can go up, and they can also go down. You need to make sure the cash flow is high enough to cover a lower rent rate in a down market. It’s best to set a standard minimum potential cash flow you’d accept before making an offer. Many investors we have worked with in the past have used the figure $400 as the minimum. Second, you have to make sure you have additional money for unforeseen repairs on the property; this can be as cheap as fresh paint in between new tenants or as expensive as a sewer replacement. The better you care for the home, the better the long-term investment. Third, not every property is going to make financial sense as a rental. Don’t fall in love with a home; as stated above, keep the emotion out of the transaction and focus on the numbers.

If you’re ready to jump into the exciting world of real estate investing in Denver, contact a TK Homes agent and let’s get to work. To help you get started today, download our free cash flow calculator below. Simply fill out each field and start seeing potential cash flow for any property.

~ Written by CEO/REALTOR® Trevor Kohlhepp

Get the »

TK Homes Blog

Share this page »